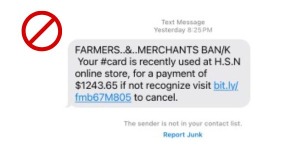

We have been made aware of an unsolicited text and phone call scam circulating through our area. In reported cases, a customer received a text message that appears to be from the F&M

Bank fraud department, or other local financial institutions. The text message references a purchase from an online store, in many cases “H.S.N online store”, and asks for the customer to select a link to cancel the transaction. A sample is to the right for your convenience.

Please DO NOT click any links sent to you via text.

Unfortunately, fraudsters can configure a text message or phone call to appear to come from any source. This scam is extremely dangerous because it seems legitimate. To best protect yourself, never give out your confidential information over the phone or via text.

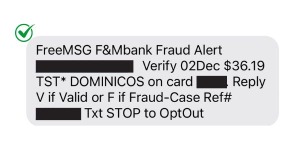

Our fraud detection services will text, email, or call clients if a transaction is suspicious; however, our platform will not request that you select a link to cancel a charge. Our fraud services will only ask that you confirm if you initiated the transaction with a simple “V” for Valid or “F” for Fraud response. See below for an example of a valid fraud alert.

Stay safe and alert

If you receive such a call or text message, do not respond. Contact your local F&M Branch using a number you know to be valid. Do not use numbers contained in the caller ID on your mobile phone.

“Regularly monitor your bank and credit card accounts for any unauthorized transactions. Be sure to install F&M Mobile on your mobile device to monitor your accounts and receive alerts while on the go!

Set up transaction alerts to receive notifications whenever a transaction is made. Report any suspicious activity to your financial institution immediately. Purchase alerts are customizable, can be received via email or text, and can be used to confirm legitimate purchases or notify you of suspicious activity. F&M Bank allows you to set transaction and balance alerts within F&M Mobile and Online Banking to stay on top of unexpected transactions on your account.”

Are you looking for a new bank? Still trying to decide if it’s time to make a switch? There are a variety of options out there, including online-only and brick-and-mortar banks. Admittedly, we’re a bit biased, having served the Shenandoah Valley with brick-and-mortar bank offices since 1908. In this article, we’ll explain what a brick-and-mortar bank is, what an online bank is, and what the primary differences between them are. Keep reading to decide between online banks vs. brick and mortar.

What is Considered A Brick-And-Mortar Bank?

When we say brick-and-mortar bank, we mean the physical branch you probably think of when you hear “bank.” You can drive to a brick-and-mortar bank, come inside for lobby service, or use the drive-thru, all with friendly human employees to help with whatever you need.

Brick-and-mortar financial institutions come in all shapes and sizes such as community banks and credit unions, or larger regional and national banks. While they offer online and mobile banking services, brick-and-mortar banks are distinguished by their branch networks. Customers of these financial institutions can bank however they like–digitally, on the go, or in person with the tellers and loan officers at their nearest branch.

What Is Considered An Online Bank?

With “Internet banks,” there are no branches to visit because they operate exclusively online. Since they don’t have overhead costs associated with operating branches, online banks may offer lower-cost or free banking, plus higher-than-average interest rates. However, they usually have a more limited menu of bank accounts, loans, and services. And, if you need help, you

won’t be able to meet with a human employee in person. Instead, customer service is handled by phone, email or chat, and banking is done through a website or usually an app

Benefits of a Traditional Bank

Why choose a traditional, brick-and-mortar bank over an online-only financial institution? Here are the top benefits of traditional banking:

● Invested in your community because we are part of the local economy.

● The more successful our personal and business customers are, the more successful our bank is.

● Get to know the bankers and tellers at your local branch. We know your face and your name and can sit down with you for in-person assistance anytime you need it.

● Some banking services–such as cashier’s checks, money orders, notary services, and safe deposit boxes–are only available at a brick-and-mortar branch.

● It’s easy to deposit funds in whatever way is easiest for you–mobile check deposit or cash or check deposit at the branch, drive-thru, or ATM.

● Enjoy access to a large ATM network you can make fee-free withdrawals from.

● Choose from the widest variety of personal and business bank accounts, loans, and services.

Upsides of an Online Bank

Are traditional and online banks really that different? Let’s compare benefits:

● Generally charge lower or no fees for products and services.

● Many traditional banks now offer fee-free services and products, such as free checking.

● Online banking can save you time and trips to the bank.

● Most brick-and-mortar banks offer online and mobile banking apps with all of the latest features, letting you combine the benefits of both in-person and digital banking.

● Because they don’t have to pay the overhead of physical branches, online banks can offer higher interest rates for some accounts.

Downsides of an Online Bank

Are the perks of an online-only bank worth the potential downsides? We’ll let you decide…

● No physical branches to visit if you want to take out or deposit cash or get in-person help.

● Customer service is only online or over the phone, which can be frustrating at times.

● Unless the bank is connected to an ATM network that accepts cash–and you’ll usually have to go out of your way to access this ATM–you cannot make cash deposits.

● Transactions, such as deposits, may take longer to clear with an online bank.

● No extra services like document notarization, safe deposit boxes, or financial advisors.

● Must be comfortable with using the Internet and/or a mobile app. With online banking, all tasks are done online and require an app and Internet connection.

● Not connected to your local community, or to any community really.

About F&M Bank

Founded in 1908 to serve farmers and merchants in Western Virginia, F&M Bank is headquartered in the Shenandoah Valley, with a network that spans the I-81/I-64 corridor from Winchester to Waynesboro and beyond. We are committed to the success of the ag industry, small businesses, and the non-profit sector. Visit us at your nearest branch location, make an appointment with a banker, check out our digital banking options, or send us a chat message within the F&M mobile banking app.

https://www.fmbankva.com/wp-content/uploads/2024/04/AdobeStock_203814562.jpeg15002000Kristen Durkee/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgKristen Durkee2024-04-03 09:18:442024-04-03 09:18:44Why Choose A Brick-And-Mortar Bank in Virginia?

Charitable organizations are exempt from paying state and federal income taxes, but that doesn’t mean you don’t have to file anything with the IRS each year. In this article, we’ll explain how to obtain 501(c)(3) status, what information is required for a 501(c)(3) tax return, and how and when to file one. After we cover federal tax returns for non-profits, we’ll move to the state level to explain how to get tax-exempt status in Virginia and what forms need to be filed each year. If you have questions, feel free to reach out to our business banking team–we’re always here to help!

Non-Profit Tax Status

To be considered a non-profit legally for tax purposes, you must apply for exempt status as a 501(c)(3) from the IRS. The most common types of 501(c)(3) entities are charitable organizations, religious groups, private foundations, some political organizations, and others such as civic leagues, social clubs, and more.

To earn tax-exempt status, your non-profit organization must meet the IRS’s eligibility requirements.

Cannot serve private interests.

Net earnings cannot benefit private shareholders or individuals.

Earnings can only be used to advance the non-profit’s charitable mission.

Cannot engage in activities to influence legislation or participate in campaign activities for political candidates.

Employees must be paid fair market value for their position.

Must stay faithful to the organization’s founding purpose.

To apply for tax-exempt status, there are different forms depending on the type of non-profit.

Form 1023-EZ: Charitable, religious, and educational organizations

Form 1024: Other nonprofit or tax-exempt organizations

IRS Form 990

Form 990 is the annual information return filed by tax exempt organizations, non-exempt charitable trusts, and section 527 political organizations. In addition to being filed with the IRS, these returns are usually available to the public upon request. The information on form 990 can shape public perception of an organization. This includes the organization’s activities, finances, governance, and more. While all exempt organizations must complete Parts 1-7 of Form 990, additional schedules may be required depending on the type of organization and its activities. The most common types are:

990-N (e-Postcard): For organizations with gross receipts not exceeding $50,000. The eight-question online form allows you to quickly record data. Asks for EIN, Tax Year, legal name and address, principal officer name and address, URL, and confirmation of tax receipts under $50,000.

990-PF: For private foundations, regardless of financial status. Requires a report on private assets, trustees and officers, grants, and financial activities.

990-EZ: Organizations with gross receipts less than $200,000 and total assets less than $500,000. The four-page form includes a statement of financial position, record of projects and accomplishments, itemized grant information, membership dues, salaries, occupancy and rent, printing and publications, and more.

990: Gross receipts at or above $200,000, or total assets at or above $500,000. The 11-page form includes the organization’s mission, number of voting members, details of the organization’s program service accomplishments of the three largest program services by expense, list of officers, directors, trustees, key employees, and highest compensated employees, as well as a full report on expenses

On every type of form, you can expect to provide the following information:

Your organization’s mission statement

Financial details such as revenue, expenses, liabilities, and assets

All activities (including any new program services) carried out throughout the year

Names and information of staff, directors, managers

Accomplishments to validate tax-exempt status

As of July 2019, with the Taxpayer First Act (Provision 3101), the 990 forms must be filed online.

Non-Profit Tax Return Deadlines

Non-profit tax forms are due on the 15th day of the 5th month after the conclusion of the organization’s fiscal year. If you operate on the calendar fiscal year, your due date would be the 15th of May. If you can’t make that deadline, you can file Form 8868 to request a six-month extension. It’s generally recommended that organizations file for an extension if they plan on conducting a financial audit.

Penalties For Late Filing

Receipts less than $1,000,000: $20/day if the return is late. The max penalty is $10,000 or 5% of gross receipts, whichever is less.

Receipts more than $1,000,000: $100/day if the return is late. The max penalty is $50,000 or 5% of gross receipts, whichever is less

If you fail to file three years in a row, you run the risk of your 501(c)(3) status being revoked.

How To File a Non-Profit Tax Return

As stated above, non-profit tax forms must be filed online. We recommend hiring an accountant or tax professional to help you ensure accuracy. When hiring a tax advisor, follow these tips:

Look at pricing, hidden fees, and expenses.

Has the accountant worked with similar organizations? They will have more experience and expertise to work through your forms.

Check their reviews and recommendations.

Virginia State Tax Filing For Non-Profits

To qualify for exempt status in Virginia, you must meet the following standards:

Be exempt under Sections 501(c)(3), 501(c)(4), or 501(c)(19).

Show proof of compliance with Virginia law for organizations that solicit contributions in the Commonwealth.

The organization’s annual administrative costs, including salaries and fundraising, must not exceed 40% of its annual gross revenue.

If your organization’s gross annual revenue is at least $750,000, you must provide a financial review done by an independent CPA.

If gross annual revenue is at least $1 million, a financial audit may be required instead of a financial review.

Once you have exempt status for Virginia tax purposes, follow these steps to file a state return for your non-profit.

First, file Form 990 with the IRS.

Then, file Virginia Corporate Tax Returns (Form 500) if your organization has unrelated business income.

Next, file Virginia Sales Tax Exemption Renewals (Form NP-1)

We are headquartered in the Shenandoah Valley, with a network that spans the I-81/I-64 corridor from Winchester to Waynesboro and beyond. Founded in 1908 to serve farmers and merchants in Western Virginia, we are more committed than ever to the success of the ag industry, small businesses, and the non-profit sector. Check out our checking account for non-profits with our Local Promise Deposit Account Package. We offer a variety of services to help you run your non-profit efficiently and effectively. For more information on non-profits, check out our Guide to the Best Non-profit Resources in the Shenandoah Valley and Beyond!

https://www.fmbankva.com/wp-content/uploads/2024/02/AdobeStock_448123379.jpeg13332000Kristen Durkee/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgKristen Durkee2024-02-23 13:54:522024-02-23 13:54:52Filing a Non-Profit Tax Return

Maybe you just got married or moved in with a long-term partner. Or you’re starting a business with other people. Perhaps you’re suddenly in a caregiver role for an aging parent or trying to figure out the easiest way to share spending money with your kid at college. These are all situations in which sharing a bank account could be helpful and convenient. However, there are also potential downsides to shared bank accounts. In this article, we’ll walk you through everything you need to know about joint bank accounts for couples and other types of relationships.

What Is A Joint Bank Account?

A joint bank account is a checking or savings account that two people share ownership of. The joint owners have equal control over and access to the account. While joint bank accounts are common among married couples, this type of account can be useful to other types of relationships as well, such as unmarried, co-habitating couples; a parent and child in college; a senior and their caregiver relative; business partners; and more.

With a joint bank account, all owners named on the account can access the funds, meaning withdraw cash, write checks, and make online bill payments and everyday purchases with a debit card. Some transactions may require both signatures. The joint accountholders also share equal responsibility for any fees or charges.

So, a basic foundation of trust and cooperation should be established before opening a joint bank account. Joint budgeting is also a good idea for a joint checking account. You may even want to create a set of rules for both accountholders to abide by.

Benefits of a Joint Bank Account

Is a joint bank account right for you? The answer will depend on your specific situation. Learn about the potential advantages of having a joint bank account to see if it could benefit your relationship.

Couples can use a shared checking account as a way to pay household bills and expenses from pooled funds.

Parents can have a joint account with their older teenagers or college-age kids to provide financial assistance and help them learn how to budget and manage funds responsibly.

Seniors can add one or more of their adult children to a joint bank account to help them manage bills, everyday purchases, and other routine banking tasks.

Having a joint account comes with certain privileges upon the death of one of the owners: “Rights of Survivorship” means all funds will pass to the surviving owners, and the account will be considered an individual account. And “Tenancy in Common” means that, if one accountholder passes away, their share of the account passes to their estate.

Downsides To a Joint Bank Account

Of course, there are some potential pitfalls that come with sharing a bank account. Review these downsides so you can determine if a joint bank account will work for you.

Trust can be an issue–one accountholder’s spending habits affect the other, so trust may be broken in the course of sharing a bank account.

Depending on your tax situation (self-employed, business owner, etc.), sharing a bank account can make tax time more complicated.

Divorce can also complicated shared accounts, especially if one spouse tries to withdraw more than half of the shared funds.

When sharing an account with a teen or young adult child, you want to set them up for future independence, not have them become too reliant and comfortable with the ease of having parents add funds to the account

Both accountholders can view all transactions in the joint account, which takes away privacy. Even if you and your partner agree on how much discretionary spending money you each get, you may not want each other to know about every single purchase.

Joint accounts are susceptible to paying any debts and court orders, like child support, back taxes, or garnishments

Should I Have an Individual As Well As a Joint Bank Account?

Luckily, it’s not an either/or choice between having a joint or individual account. You and your partner or child can have multiple bank accounts. For example, many couples maintain a joint account for shared household expenses, but also keep their own individual accounts for discretionary purchases. That way, your partner doesn’t need to know how many fancy coffee drinks you buy in a week. Keeping your own individual bank account also allows you to set aside money for gifts and surprises

You can always link your shared and individual accounts to make it easy to move money back and forth, while still preserving privacy and independence.

Finally, it’s not fun to think about, but if things go south in your romantic or business relationship, already having an individual account will make it easier to separate finances and assets.

How to Open a Joint Bank Account

Opening a joint checking or savings account follows the same process as opening an individual account. You just need to provide information for both the accountholders. At F&M Bank, you can conveniently open an account online or visit your nearest branch location in the Shenandoah Valley. When prompted, simply enter the additional applicant information. Before you get started, collect basic information for all account holders such as addresses, dates of birth, ID information, and Social Security numbers. During the set-up process, you can decide on alerts and other settings for one or both accountholders.

https://www.fmbankva.com/wp-content/uploads/2024/02/AdobeStock_470157695.jpeg13332000Kristen Durkee/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgKristen Durkee2024-02-12 09:21:282024-02-12 09:21:28Is A Joint Bank Account Right For You?

Even before your baby is born, you’re probably thinking about the financial changes a child will bring. New parents have to revise their household budgets to account for expenses like diapers, clothes, childcare, and more. You may also want to start saving for college now. But don’t forget to include your child in financial habits and literacy. Kids learn behavior from their parents, but they can’t learn anything about money if you don’t teach them and model good habits. In this article, we’ll discuss personal banking for kids and how to develop good habits from birth through college.

Start Early With Savings

The earlier you start saving, the more time your money has to grow. Even little amounts will add up over time. This is due to Compound Interest, which is when you earn interest on your initial deposit as well as the interest you accumulate. You can use this Compound Interest Calculator to show your child how much a deposit to their savings account now will grow over a certain number of years.

Building the savings habit will also help your child learn good money habits, such as delayed gratification. Saving also teaches the concept of financial planning–we are putting money away for a rainy day, for example, or saving for a specific purchase or expense.

To help your new baby or young child get an early start on savings, you could open a custodial account or start a trust fund. Both types of accounts give you control over when your child will have access to the funds. Consult with your tax advisor about the tax implications of a trust or custodial account.

Open a Youth Savings Account

Let your child in on the fun! Kids savings accounts are a type of joint account–both you and your child must be on the account, so take them to the bank with you and let them participate in opening the account. You can also take them to deposit funds and use the coin counter machine. Make banking fun so your child will take an interest and want to continue with saving as they get older.

Our Treehouse Club is a special savings account for kids aged 6-18. It comes with a piggy bank for saving at home, a passbook for recordkeeping, and a prize every five deposits. There are no minimum balance requirements or service fees. Learn more about the perks and benefits of Treehouse Savings.

Learn About College Savings Accounts

In addition to general children’s savings accounts, parents can open a college savings account to prepare for future educational expenses. Even if your child ends up taking a different path, the funds can be used for a sibling’s college education. These educational savings accounts can also be used for K-12 private and religious school costs. A college savings account can also be closed and the funds disbursed, although tax penalties will apply.

Also known as a qualified tuition program (QTP), each state has its own 529 plan to help residents either prepay for college tuition or save for higher educational expenses.

Earnings on your 529 plan accumulate tax free while in your account. Withdrawals for qualified higher education expenses are not taxed. 529 plan funds can also be used to make payments on the beneficiary’s or a sibling’s student loan (limited to $10,000).

If your child doesn’t use all of the balance for educational expenses, and there is no sibling to transfer funds to, you can close the account and use funds for other expenses–subject to a tax penalty and other terms.

Contribute up to $2,000 per year and enjoy tax-free withdrawals for qualified educational expenses.

Kids’ Checking Accounts

As your child gets older, they may start working to earn their own money. And they may want to spend some of the money they’ve been learning to save. This is the time to open a checking account for your teenager. Learning how to manage a checking account is an important part of financial literacy and well-being. They can use a debit card, keep track of the money coming in and going out, and reconcile their account to avoid overdrafts. As your teen accumulates some of their own expenses, such as a car or cell phone, they can also learn to budget for monthly income and expenses. Remind them that “saving should always be your biggest expense.”

Financial Responsibility

As your child gets closer to adulthood, it becomes more and more important to teach them financial responsibility. As they grow, you can build upon lessons you taught them when they were young.

Teach budgeting with an allowance. Kids know how much they will get each week and can decide what to spend and how much to save.

Incentivize saving. Show your kids their savings account statement so they can see compound interest in action. Offer a “match,” such as one dollar or a few dollars for their savings deposits.

Encourage generosity. Have your kids contribute to a family donation to a local charitable cause. Ask them to use their own money to buy holiday or birthday gifts for a sibling or other relatives.

Talk about spending as a series of choices. Instead of saying “we can’t afford that,” you can say “we’re choosing to use our money for ___ instead.”

Offer opportunities to earn more. Whether or not you require chores for your child’s regular allowance, you could offer occasional chances to earn extra money for help around the house.

Explain how debt works. Your kids may see you using a credit card to pay at a store and think that money is “free” or “grows on trees.” Talk to them about how you pay off your credit card charges each month or, if you don’t, your credit card will charge a high interest rate to carry a balance and that interest compounds, too.

Open a savings account for your child!

Set your child up for future financial success by opening a college savings account. At age six, take your kid(s) to your local F&M Bank branch in the Shenandoah Valley, Virginia, to open a Treehouse Savings Club account. Have questions about youth savings accounts or other aspects of your family’s finances? Give us a call or visit your nearest branch location.

https://www.fmbankva.com/wp-content/uploads/2023/07/AdobeStock_91085192.jpeg14872000Kristen Durkee/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgKristen Durkee2023-07-14 16:19:062023-07-14 16:19:06Teaching Kids About Money: From Birth To College

F&M Bank’s Chief Experience Officer, Charles Driest, talks about striking the right balance between digital innovation and a personal customer approach

Charles Driest is the newly-appointed Chief Experience Officer at Farmers & Merchants (F&M) Bank. A graduate of George Mason University in Virginia, and later St. John’s University in New York, he began his banking career shortly after returning to Virginia from New York in 2007.

Before this, Driest’s early career saw him employed by the Grocery Manufacturers Association (MGA), and, later, at the American think-tank, Brookings Institution. It was here he was struck with inspiration to retrain in finance by a former manager, Roberta Cohen.

Driest says: “She said if I didn’t go back to school she would fire me. This was probably my biggest inspiration. It amazes me that her voice is always in the back of my head, and when she told me that, it was about two decades ago.”

F&M Banks’s new Chief Experience Officer hasn’t exactly been short of inspiration, either: “I’ve been really lucky because I’ve had a lot of influencers in my career, with bosses and managers who have pushed me to take on new risks that perhaps I didn’t feel I was ready for, but gave me a great opportunity to learn.”

Beginning his banking career after reeducating in New York and returning to Virginia, Driest was again inspired to follow a digital path in his career. “One of the first CEOs I worked for taught me a valuable lesson; it’s how I got into the digital side of the banking business.

“At the time we didn’t have a good grasp of our digital spending at the organisation. My CEO asked me to break down the numbers to explain to executive management where the money was going. So I sifted through 12 months of invoices and began asking operational questions: where’s our money going? How do we better manage this?

“This is when I found out the business had these operational holes, while we didn’t have the right insights into the capabilities available to us that we were using. So my CEO said: ‘You found the problems, go fix them’. This is what got me into digital banking, furthering my career by putting me into a situation I wouldn’t necessarily have been comfortable in initially.”

This valuable experience in digital banking saw Driest become F&M Bank’s Director of Digital Banking sometime after, a role he had for “14 to 15 months” before being promoted to F&M Bank’s Chief Experience Officer.

Despite his brief time in the role so far, Driest says: “Taking on three new reports has been a lot of fun. I really enjoy the personnel management aspect of things. I like watching the development of people. From my perspective, I really like to see the process of a team getting onto one page, because it has a powerful multiplying effect. The pace of work speeds up when everybody is in sync.”

Achieving synchronisation for the now is key to driving growth in the future, according to Driest, who has deep excitement for the future of banking as the proliferation of fintechs continues, believing community banking will endure despite the growth of technology.

He concludes: “I’ve seen some of the biggest developments in banking over the years, and I feel even with all the fintechs out there, I think ultimately, community banking will survive. If there’s one thing banks are very good with, it’s about integrating technology that is focused on the customer.

“For anyone that talks about the speed of fintech growth, fundamentally, it still relies on people, and people don’t change habits that quickly. The arc of change and the pace of change will always be constrained by people at the end of the day. So, as long as you’re making good decisions and always looking ahead by two to three years at a time – it doesn’t matter what type of bank you are – you’ll probably end up in a good place.”

F&M Bank has been featured in the July issue of FinTech Magazine

In this exclusive interview, Charles Driest, Chief Experience Officer, discussed striking the right balance between digital innovation and a personal customer approach.

“The future is technology and people, that’s what is going to win the day – not one or the other”

BizClik’s FinTech portfolio connects banking, financial services, payments, technology & consulting brands and their most senior executives with the latest FinTech trends, industry insight, and influential FinTech, InsurTech & Crypto projects as the world embraces CX, Business Transformation and Digital Ecosystems. FinTech Magazine and its entire portfolio is now an established and trusted voice on all things FinTech, engaging with a highly targeted audience of 113,000 global executives. We provide key industry players with the perfect platform to showcase their brands, develop content syndication plans, webinars, white papers, demand generation as well as a global set of events (In-Person & Virtual).

BizClik is a UK-based media company with a global portfolio of leading industry, business and lifestyle digital communities.

BizClik’s portfolio includes Technology & AI, Finance & Insurance, Manufacturing & Supply Chain, Energy & Mining, Construction, Healthcare, Mobile & Data Centres and EV. For further information, please visit https://www.bizclikmedia.com/

You can read the report in the latest issue of FinTech Magazine by clicking HERE

About F&M Bank F&M Bank Corp. (OTCQX: FMBM) proudly remains the only publicly traded organization based in Rockingham County, VA, and since 1908, has served the Shenandoah Valley through its banking subsidiary F&M Bank, with full-service branches and a wide variety of financial services, including home loans through F&M Mortgage, and real estate settlement services and title insurance through VSTitle. Both individuals and businesses find the organization’s local decision-making and up-to-date technology provide the kind of responsive, knowledgeable, and reliable service that only a progressive community bank can. F&M Bank has grown to $1 billion in assets with more than 175 full- and part-time employees. Its conservative approach to finances, sound investments, and excellent customer service have made F&M Bank profitable and continues to pave the way for a bright future.

###

https://www.fmbankva.com/wp-content/uploads/2023/07/FM-Bank-Social-July20233.jpg10462000Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2023-07-10 14:35:352023-12-05 17:16:51F&M BANK: DRIVING DIGITAL WHILE STAYING PERSONAL

F&M Bank leverages Jack Henry security, operational efficiencies and open banking infrastructure to support growing retail and commercial accounts

Press Release Courtesy of Jack Henry & Associates, Inc.

MONETT, Mo., March 28, 2023 /PRNewswire/ — Jack Henry™ (Nasdaq: JKHY) announced today that it is expanding its existing partnership with longtime client Farmers & Merchants Bank (F&M Bank), a $1.25-billion asset community bank based in Virginia. While larger financial institutions have left the area, F&M Bank is leveraging Jack Henry’s modern technology architecture to serve the market in need with scale and efficiency.

The bank is committed to providing the communities it serves with innovative, convenient and reliable retail and commercial services. Jack Henry’s Banno Business will help the bank expand its business and agricultural accounts to larger markets. In addition, the bank will be deploying treasury management services to meet the most advanced business needs.

Founded in 1908, F&M Bank has been providing personalized banking services and financial solutions to individuals and businesses across Virginia for more than a century. The bank has built a reputation for its commitment to customer service, community involvement, and agricultural lending in the Shenandoah Valley area. F&M Bank has invested in the fintech ecosystem by joining BankTech Ventures, and furthering its dedication with Jack Henry’s open infrastructure will support the evolving needs of its community by providing access to a wider range of financial services.

“F&M Bank has met the banking needs of our communities for 115 years with exceptional customer service and innovative products and solutions,” said Mark Hanna, Chief Executive Officer & President of F&M Bank. “Jack Henry understands that it is community banks like F&M Bank that power Main Street America. We share a vision for the future where technology and people will equip us to grow and scale. We have partnered with them to drive the continual improvement of features, functionalities, and security that will help ensure that our accountholders have faster and better modern services. Together, we are positioned to continue forward while maintaining a focus on our customers who make it all possible.”

Stacey Zengel, senior vice president of Jack Henry and president of Bank Solutions, said, “Jack Henry is committed to ensuring that financial institutions like F&M Bank will continue to be pillars of innovation and financial opportunity for the communities they serve. The bank has been a part of financial lives in the Shenandoah Valley for generations, and with modern, user-friendly, scalable services, they will be able to reach many more generations to come.”

About Jack Henry & Associates, Inc.®

Jack Henry™ (Nasdaq: JKHY) is a well-rounded financial technology company that strengthens connections between financial institutions and the people and businesses they serve. We are an S&P 500 company that prioritizes openness, collaboration, and user centricity – offering banks and credit unions a vibrant ecosystem of internally developed modern capabilities as well as the ability to integrate with leading fintechs. For more than 46 years, Jack Henry has provided technology solutions to enable clients to innovate faster, strategically differentiate, and successfully compete while serving the evolving needs of their accountholders. We empower approximately 8,000 clients with people-inspired innovation, personal service, and insight-driven solutions that help reduce the barriers to financial health. Additional information is available at www.jackhenry.com.

SOURCE Jack Henry & Associates, Inc.

https://www.fmbankva.com/wp-content/uploads/2023/03/iStock-1325967831.jpg8142000Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2023-03-28 10:01:192023-05-05 15:07:24F&M Bank Expands Longtime Partnership with Jack Henry

With the cost of homes up 10% since last year in Shenandoah County, and interest rates continuing to rise, many buyers are exploring options for reducing the compounding impact of high interest rates on already high home prices. Many are considering 2-1 buydown mortgages, where interest is prepaid, temporarily lowering your monthly payments, before returning your official interest rate after two years.

On the surface, during times of higher interest rates, getting a 2-1 Buydown mortgage might make sense—especially if you expect your income to rise in the future, as your interest rate rises. Unfortunately, with a 2-1 buydown, those high interest rates we experience today will be permanent for the remaining life of your loan after just two years. And the Federal Reserve has recently indicated that they may begin to lower the Fed Funds rate in 2024, which often means lower interest rates down the line.

A popular alternative to 2-1 temporary buydowns is the adjustable-rate mortgage (ARM). Like a temporary buydown, you will start with a lower rate for a set duration (the most popular introductory rate length is 5 years), then reset to the market rate down the line, fluctuating each year thereafter. When rates are high but are likely to fall, these mortgage products can be a smart economic choice. But when does it make sense to get an ARM over a 2-1 buydown on a conventional thirty-year loan? In this blog we will break down the differences between 2-1 buydown mortgages and ARMs and discuss advantages and disadvantages, to help you make an informed decision on which mortgage products would be the best choice for you.

What is a 2-1 buydown mortgage?

A 2-1 buydown mortgage is simply a fixed-rate mortgage where part of the interest is prepaid for the first two years, temporarily lowering monthly payments. The seller, builder, or in some cases the buyer pays to have the payment effectively reduced during this time, usually by depositing the prepayment in an escrow account. When funds for the buyback come from the seller or builder, it’s considered a ‘seller assist’.

Even if you take advantage of a 2-1 buydown mortgage, it’s important to note that everything else about the loan remains the same: your down payment amount will not change, you will need to have sufficient income to qualify for the full payment (the one that kicks in at year 3) at the time of application, and other closing costs (which average 1.74% for the buyer in the state of Virginia), will be unaffected by the buydown. And not every mortgage product can be used in conjunction with a 2-1 buydown. While conventional, 30-year fixed rate loans (‘conforming loans’) are prime candidates for a temporary buydown, if you are pursuing a nonconforming home loan product, like a VA or FHA loan, you’ll need to speak to your lender to see if it qualifies. And most lenders will only accept buydowns on fixed-rate loans—in other words, you can’t combine them with an ARM.

So, how exactly does a 2-1 buydown work?

Usually, a builder or seller uses a temporary buydown as an incentive for buyers to purchase a home, paying a lump sum into an escrow account to cover the difference in monthly payments for years one and two. Less often, a buyer with extra cash will utilize a buydown to reduce their monthly payments, though buyers often purchase ‘discount points’ for a permanent buydown (where the actual rate is reduced for the life of the loan), instead.

In the first year the monthly payment is what it would be if your mortgage rate was 2% less than the actual interest rate. In the second year, this prepayment is equal to a 1% rate reduction. In years three through the rest of the mortgage, the payment reverts to what you would pay with your actual interest rate. For example, if you have a mortgage with a 7% interest rate, in the first year your payment would be equal to a payment with a rate of 5% (i.e., 2% reduction). In the second year, it would equal that of a 6% mortgage interest rate (i.e., a 1% reduction). And in year three, your payment would rise and remain at the official 7% rate.

How does an ARM work?

With an adjustable-rate mortgage your interest is locked in at a low rate initially. Then, after a set term, it will fluctuate each year thereafter, based on market rates. While the numbers in a temporary buydown refer to the reduction of interest points in year one (2 percentage points) and year two (1 percentage point), the first number in an ARM refers to how many years your rate is locked, and the second number refers to how often it can change after that. A 3-1 ARM is locked for 3 years, but after that period it can change once per year based on market rates. Likewise, a 5-1 ARM is locked for 5 years, and a 7-1 ARM is locked for 7. The most common form of ARM is the 5-1 ARM.

When interest rates are low, an ARM might be considered a more risky mortgage product. This is because instead of locking in a low interest rate for the life of the loan, borrowers get an even lower rate for a few years, but then are at risk for large increases in monthly payments, should market rates go up. If rates go up significantly, your mortgage could become unaffordable for you. And if you choose to refinance, you’ll have to refinance at higher rates, even if you choose another ARM.

However, when interest rates are high, ARMs make a lot more sense. Not only do you lock in an initial rate that’s lower than the market rate—potentially saving you a lot of money on interest—future interest rates are less likely to increase too much over your initial rate. After the introductory period is up (or sooner!), you can also consider refinancing your loan if rates come down significantly.

Let’s take a look at a sample 5-1 ARM scenario compared to a 2-1 buydown mortgage to see how much you could save in the first five years.

Our homebuyer is interested in purchasing a house with a budget of $300,000—just shy of the recent median listing home price of $302,500 in Shenandoah County, VA. She is comparing two potential options: a 5-1 ARM at a rate of 5.5%, and a 2-1 buydown mortgage at a 6.5% interest rate. She plans on putting 20% ($60,000) down.

With a 5-1 ARM, her monthly payments would be set at $1,363 for the first five years of her loan. Total payments including interest and principal during this time would equal $81,780. After the initial five-year period, her rate will fluctuate annually based on the current market rate, or she could choose to refinance to a permanent lower rate if available.

With the 2-1 buydown mortgage, in the first year her mortgage payment would be $1,216 each month, rising to $1,363 in year two, and settling into $1,517 in the third year. Her total principal and interest payments for this five-year period would equal $85,560. Keep in mind that the ultimate higher monthly payment will continue through the life of the loan.

Benefits of a 5-1 ARM over a 2-1 Buydown Mortgage

In addition to saving money on overall loan interest and loan payments, 5-1 ARMs can have other advantages over temporary buydowns. Here are a few ways you can benefit from utilizing a 5-1 (or other) ARM:

Reduced monthly payments for a longer term. As we mentioned above, the biggest benefit of a 5-1 ARM is that you will receive a reduced interest rate for a full five years (60 months), before your mortgage sets to the current market rate. With a 2-1 buydown, your rate climbs after the first year, before hitting the full interest rate at year 2.

Greater stability in the near term. While ARMs will fluctuate more often after the first five years than a 2-1 buydown, in those first five years of your loan your rate and monthly payment won’t change. As you are recouping the savings you put toward your down payment, closing, and moving costs, not having to worry about rising rates within the first year can be helpful to buyers—especially those who are just starting out.

More money for other expenses. The first few years are when homeowners typically invest the most in their new housing. In fact, according to a survey by the National Association of Home Builders, in the first year alone homeowners spend over $13,000, with an additional $7,000 in year two.

Reduced impact of high interest. Especially with today’s record high rates, even a temporary interest reduction can help you offset your first few years of homeownership and replenish those savings you spent on your down payment and closing costs. However, if you have reason to believe interest rates will come down in the future, that can lead to even further savings—particularly if the alternative is locking in a high-interest 30-year mortgage.

No pressure to secure seller assist financing. A 2-1 buydown requires securing some sort of seller assist financing from the current owner or builder—and they are often used to attract buyers in slow markets. But in tight, competitive markets, you have a much lower chance of scoring this perk—and they sometimes come at the tradeoff of a higher price for the home itself. With a 5-1 ARM, you are in control. You can get a 5-1 ARM in any housing market, and aren’t reliant on the seller or builder to get your initial reduced interest rate.

Dangers of the 2-1 Buydown Mortgage

While 2-1 buydown mortgages do have a similar benefit in reducing your initial monthly payments, they do come with some potential pitfalls. If you go down the path of a temporary buydown, these are some things to watch out for:

Getting too comfortable with lower monthly payments. While you do need to be approved for the actual interest rate and payments with a 2-1 buydown, if you get used to the lower payments in year one—and even in year two—it can be hard to adjust your spending levels when your payments rise in the third year, putting you at risk of overspending or not being able to afford your payments.

Refinancing doesn’t pan out. If you get a 2-1 mortgage thinking you will refinance before your higher rate kicks in down the line, keep in mind that refinancing isn’t a guarantee. Rates could be just as high, or not low enough to offset the cost of restarting a new, 30 year loan with a new amortization schedule and all new closing costs. Additionally, refinancing may require another down payment, depending on your lender and the appreciation of your home. All these factors can be a deterrent for borrowers, meaning refinancing isn’t always something you can count on.

Still need to pay PMI on top of payment increase. PMI (private mortgage insurance) is required for home loans where the borrower has not paid off 20% of the home’s value. If you don’t put 20% down at closing, this fee (usually up to about 1.5% of your loan) will be part of your monthly payment. Many people getting 2-1 buydowns who don’t put 20% down may hope to hit that mark within the first few years, eliminating their monthly PMI by the time their higher rate and higher payments kick in. But if you don’t, keep in mind your PMI fee will be added on top of your note rate increase. If you are getting a monetary seller assist, it may make more sense to use those funds to increase your down payment instead (more on this below).

Rates could come down. This is perhaps the biggest drawback of 2-1 buydown mortgages when you utilize them when interest rates are high. If rates come down, your locked rate could be much higher than the new current market rate, meaning an ARM would have been a better choice.

How do I know if mortgage rates will change?

Mortgage rates are in constant flux, and it’s impossible to predict with complete accuracy what rates will be down the line. However, there are some economic predictors including historical rates that can give us a general idea in some circumstances.

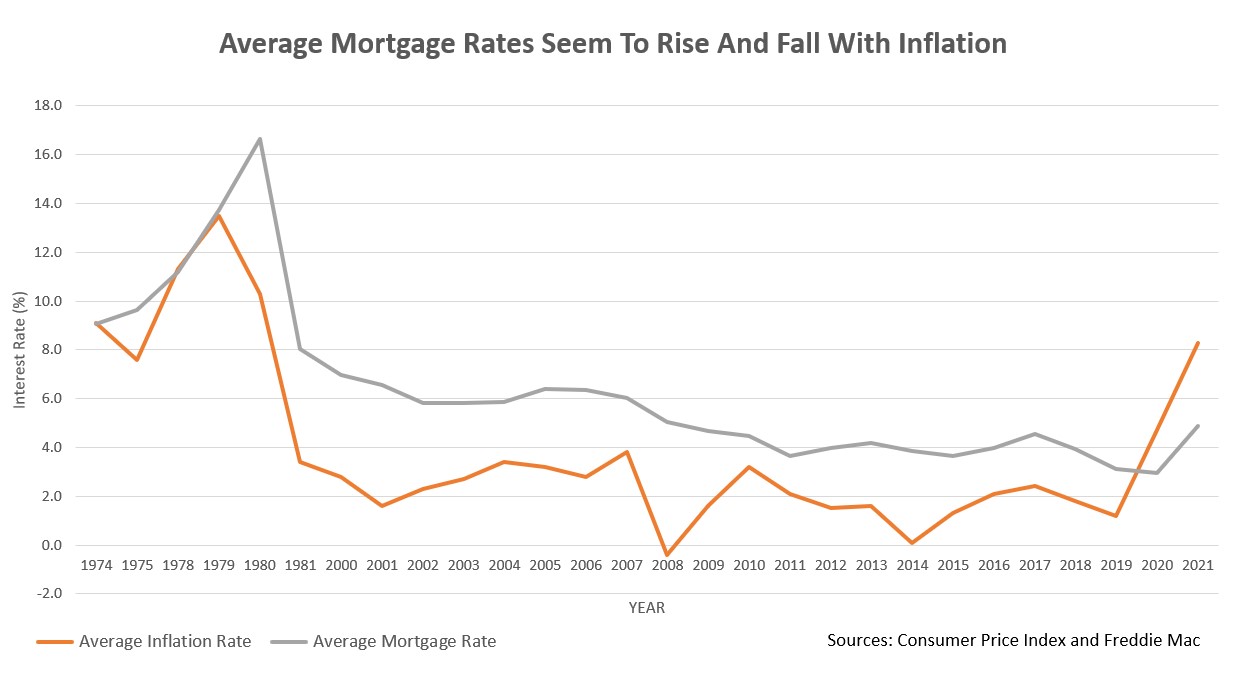

Inflation can have a significant impact on mortgage rates. That’s because when interest is low, people tend to spend more, which can result in higher levels of price inflation on goods as demand exceeds supply. The Federal Reserve’s FOMC (Federal Open Markets Committee) sets monetary policy to maintain low (or acceptable) levels of inflation—typically targeting 2-3%. The Federal Reserve takes measures to counter excessive inflation by raising their borrowing rates for overnight deposits (banks borrow from other banks’ deposited overnight reserves) during periods of high inflation. This in turn influences the rates that banks set for their own lending. Higher interest rates for consumers on home loans, auto loans, and other forms of credit ultimately slows consumer spending, bringing down inflation.

What does this mean for borrowers? Eventually, inflation will slow, prices will stabilize, and the Federal Reserve will once again lower interest rates. If rates are high due in part to inflation (as they are now), you can expect that they will likely come down again in the future. As we mentioned earlier, there seem to be strong indicators that the Federal Reserve will do just that in 2024.

But inflation isn’t the only thing that we can track to help predict future rates. Mortgage rates are affected by two other items: supply-and-demand in your residential housing market and the 10-year Treasury rate.

When fewer people are buying homes in your regional market, rates may decrease (marginally) to encourage new home purchases. That’s not to say there will be drastic interest rate differences across the country—but smaller regional differences are quite common. As Housing Wire shows, interest rates can vary across states by up to .2% on average, with Virginia having rates that tend to fall on the lower end. When local markets cool, expect lower rates to follow.

The 10-year Treasury rate can have an even greater effect on mortgage rates. Treasury notes are just one of many securities investments people can make, and are often chosen because they tend to carry very little risk. Mortgage-backed securities on the other hand, tend to offer higher yields, but carry more risk. As yields for 10-year Treasury notes rise in the face of inflation, investors for mortgage-backed securities will want to earn even more because of the associated risk. And to fulfill the demand for higher yields, interest rates will increase, to provide that additional money. In the near future, Treasury rates are expected to continue to rise. However, once inflation is under control, Treasury yields will likely fall once more, and with them, mortgage rates.

All of these economic factors can be difficult to follow and predict. The best thing to do is speak to a financial professional before making a decision on the right loan product. Although changes in rates are never guaranteed, if you believe interest rates will fall in the coming years, that might incentivize getting an ARM over a fixed-rate mortgage product.

Three Alternative Ways to Use Sellers Assist Money

If you are lucky enough to swing a seller concession, don’t feel limited to a temporary interest buydown—even if that is what the seller or builder initially offers you. There are a number of other options out there that might make greater financial sense in the loan run, including:

Increasing your down payment. Even if you choose an ARM mortgage, you can utilize a seller assist to reduce your out of pocket closing costs. You can transfer the savings on closing costs to a larger down payment to additionally reduce your monthly mortgage payments and maybe even avoid PMI altogether.

Using funds to offset moving costs, furnishings, and minor renovations. If you already have a sufficient down payment, but find your savings depleted after purchasing your home, you may want to use the seller assist to offset the many expenses you’ll encounter moving, furnishing your new house, and making small renovations to make it feel like a home.

Purchasing discount points to permanently lower your interest rate. 2-1 buydowns are temporary reductions in interest rates. However, you can purchase discount points to permanently reduce interest rates—especially when rates are high. The cost of a discount is typically 1% of your loan amount, and lowers your interest rate .25 percentage points.

Is an Adjustable Rate Mortgage right for you?

Interested in learning more about ARMs? Reach out to a mortgage professional at F&M Bank today to find out if an adjustable rate mortgage makes sense for you. Our lenders can discuss all the options available to you given your specific situation, provide hypothetical amortization schedules, and help you decide what home loan product is the best choice for you to get you in your new home.

* Results are hypothetical and may not be accurate. This is not a commitment to lend nor a preapproval. Consult a financial professional for full details. Hypothetical payment scenarios do not include taxes and insurance, which will result in a higher payment.

https://www.fmbankva.com/wp-content/uploads/2023/02/Header-home-mortgage-virginia-e1677102944734.jpeg9791370Kristen Durkee/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgKristen Durkee2023-02-22 16:46:152023-09-25 12:15:42Considering a 2-1 Buydown? Try an ARM Instead

Driving through the countryside of Shenandoah Valley, you’ve probably passed many manufactured and modular homes without realizing that these homes were not traditionally-built. With improvements over quality and style over the years, this form of housing has become an increasingly popular alternative to traditional homes. In fact, last year there were more than 1,000 new manufactured homes shipped to the state.

With quick turnaround times for new construction and low costs—merely a fraction of site-built homes—systems-built homes create valuable affordable housing opportunities for first-time home buyers, retirees, and anyone on a budget looking to find a quality home in the face of rising costs. But if you’ve decided that a manufactured residence might be the right choice for you and your family, you may be wondering how to finance your new home. Although it can sometimes be as straightforward as financing a traditional home, that’s now always the case. In this post we’ll discuss what exactly modular and manufactured homes are, why they can make good cost-effective housing choices, and different ways buyers can finance their homes, depending on their needs as well as the nature of their home. Keep reading to learn more!

What are Modular and Manufactured Homes?

Modular homes and manufactured houses are types of prefabricated construction in which homes are built off-site. These are homes that are built on assembly lines in plants or factories and transported to their permanent location. Both types of housing can save you time and money if you are looking for a new home, and fulfill an important need in the housing market. But what’s the difference between the two?

What is a manufactured home?

Previously called mobile homes, these are prefabricated homes that at one point were built on a chassis with wheels, designed to be moved from place to place—in other words, to be ‘mobile’. In 1976, HUD began to require certain safety standards for mobile homes, including a permanent chassis, at which point the term ‘manufactured’ replaced the term ‘mobile.’ Although manufactured homes can be moved, they are now usually kept in one place, and attached to permanent foundations. In fact, moving a manufactured home after installation can make it ineligible for financing (more on this below).

Manufactured homes usually come in three sizes: single-wide (750-1,050 square feet), double-wide (1,067-2,300 square feet), and triple-wide (size varies, based on configuration). While older manufactured homes suffered from high utility bills due to poor airflow and insulation, new homes can have upgraded features that make them feel and function much like a traditional home. As mentioned above, a major benefit of buying a manufactured home is the cost, making them a great option in affordable housing for older adults on a budget, low-income families, and those looking to save money without sacrificing amenities in a tight housing market. In fact, manufactured housing costs about a third of traditional housing in Virginia, on average: $117,000 vs. over $350,000.

Why is manufactured housing such a bargain? The building of these homes has become so efficient that they are able to avoid a lot of the labor and specialized material costs associated with building onsite. As Mark Bowersox (EVP of Industry Relations at the Manufactured Housing Institute) has explained, “In manufactured housing plants, the home moves down a planned path while specialized tradesmen complete each step. There are no delays in searching for suitable subcontractors or tradesman prioritizing other jobs.” Manufactured housing plants can buy materials in large quantities, further saving on costs.

What is a modular home?

Modular homes are a type of manufactured housing that are built—in modules—off site, and then assembled at their final location, on a permanent foundation. In addition to being known as ‘modular homes’, they are called by many other names, including ‘factory-built,’ ‘systems-built,’ and ‘prefab.’

While it might be easy to spot a double-wide or single-wide manufactured home, it’s often hard to tell the difference between a modular home and a traditionally-built house. Unlike other manufactured houses (which have their own building codes specific for manufactured housing), “modular homes are constructed to the same state, local or regional building codes as site-built homes,” as HUD explains.

Modular homes will also save you time and money: they cost 10-20% less than site-built homes and can normally be built from start to finish in less than four months.

What financing options are available for manufactured and modular homes?

If you are interested in purchasing a new manufactured home or modular home, you might assume you can pay for your home with a conventional mortgage. And while this is sometimes the case, financing for manufactured homes can also be a little bit more complicated than that. On the other hand, there are certain financing options available to manufactured homebuyers that are not available to those purchasing traditional homes. Here are some of your options:

Construction Loans for Modular and Manufactured Homes

Construction loans, which are short-term loans that finance the building of new houses, can make a lot of sense for when you are building your modular home. The typical construction loan chosen for modular and manufactured homes is the ‘construction-to-permanent loan,’ which converts to a traditional 30-year mortgage once the manufactured home or modular home is transported to and/or assembled at its permanent location. These loans don’t just cover the cost of purchasing the home—because they are paid out in intervals, as needed, you can use them for covering all the stages of building: buying the land, preparing the site, laying the foundation, running utilities, landscaping, and transporting and assembling the home itself. For more about our construction financing for manufactured homes, visit our Modular Home Loans page.

FHA Loans

FHA (Federal Housing Administration) Loans are great options for low- and moderate-income buyers who are looking to purchase a pre-existing home, as well as for those who will be buying land and purchasing a new systems-built house. As HUD clarifies on its Financing Manufactured Homes site, as long as the manufactured home was built after 1976 and meets certain guidelines, it can qualify for FHA loans up to $69,678 for the home and $23,226 for the lot. The requirements for qualification include meeting Model Manufactured Home Installation (MMHI) standards and local and state guidelines, and having a permanent foundation. FHA Loans are government-backed loans offered through your bank. To find out more, visit our FHA Home Loans page.

VA Loans

VA Loans, offered by the Department of Veterans Affairs, are also government-backed loans available to eligible service members, veterans, and military spouses. These loans can offer financing up to 100% (no down payment) to be used for purchasing or refinancing a manufactured or modular home, with or without a lot, as well as purchasing a new lot for an existing home, and refinancing an existing home to also purchase a lot for it. There are some specific requirements for manufactured homes to qualify for a VA loan, though. While the home doesn’t necessarily need to be ‘permanently affixed’ (on a permanent foundation), the approval of manufactured homes which are not will be based on local guidelines. And, as with all homes, it still must pass the VA inspection process.

If you are an active or retired service member or spouse, you can save up to $500 at closing with our Loans for Local Heroes Home Loan Program. For more information about how to apply for a VA Loan through F&M Bank, check out our VA Mortgage Loans page.

USDA Rural Development Loans

Low-income buyers who purchase a manufactured or modular home that meets USDA requirements may qualify for a Rural Development Loan through the U.S. Department of Agriculture (USDA). These homes must have a permanent foundation, be located in an eligible rural area on a site that meets state and local standards and be a new unit that’s at least 400 square feet. Many rural areas of Virginia qualify for USDA loans. Our USDA Rural Development Loans page has more details as well as pros and cons of using these loans to purchase your next home.

Conventional Mortgages

It is entirely possible to purchase a systems-built home using a conventional loan, if it has a permanent foundation and adequate living space, and was manufactured after 1976 (in other words, not a mobile home). Conventional loans typically have stricter lending requirements than government-backed loans, including a minimum credit score of 620-660 in most cases. However, if you and your home qualifies for a conventional loan, they tend to have less paperwork and lower interest rates, making them appealing to many buyers.

Ready to buy your new home?

If you’re looking to finance a manufactured home in Virginia, F&M Bank has you covered. We offer a variety of home loan options from FHA, USDA, and VA loans to conventional mortgages, as well as construction loans to help you streamline the process of purchasing a property and building your new home. Systems-built homes play a huge role in making quality housing affordable and accessible to residents all over Virginia. To learn more about how we can help, or to apply for financing for your new modular or manufactured home, stop by one of our locations throughout the Shenandoah Valley.

https://www.fmbankva.com/wp-content/uploads/2022/12/house-for-sale-virginia-1.jpeg400600Kristen Durkee/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgKristen Durkee2022-12-15 12:22:482024-04-26 09:29:53Financing Modular and Manufactured Homes in VA

Buying a home in Virginia is an exciting process that you have probably been looking forward to for years. If you are a first-time homebuyer, the process of choosing a mortgage lender, deciding on a mortgage type, and applying for a home loan may seem intimidating.

At F&M Bank and F&M Mortgage, we have been helping Virginians achieve their dreams of homeownership since 1908. It is our goal to make the home buying process as simple as possible so that you can focus on the fun part – moving into your new home.

F&M Mortgage is proud to offer Virginia Housing Development Authority (VHDA) loans to the members of our community. These specialty home loans are designed to decrease some of the financial barriers that keep many Virginians from achieving their dreams. In this article we will outline the different types of VHDA loans, their specific loan requirements, and the mortgage loan application process. Let’s find out if a Virginia Housing loan is right for you!

What is a VHDA loan?

The Virginia Housing Development Authority (VHDA) is a not for profit, public mortgage finance company. Founded in 1972 to help Virginians afford quality housing, the program operates using no state taxpayer money. The VHDA relies on the private purchase of Virginia Housing Development Authority bonds to fund its loan and grant programs. The VHDA focuses on providing loans to first-time homebuyers and developers who build quality rental housing. Virginia Housing is currently celebrating their 50th anniversary and has helped over 240,000 Virginia families afford homes.

How does a VHDA home loan work?

While VHDA loans are targeted for first-time homebuyers, some loans are appropriate for repeat homebuyers as well. In order to help the most people with the most need, VHDA eligibility includes an upper limit on both the borrower’s income and the home price. VHDA loans are designed for borrowers with low to moderate incomes. Virginia Housing loans are 30-year fixed-rate loans with a low 3 percent down payment requirement. The VHDA also offers grants to help Virginians afford their down payments and closing costs.

What are the benefits of getting a VHDA home loan?

If buying a home seems financially out of reach, consider a VHDA home loan. F&M Mortgage offers VHDA loans because we support Virginia Housing’s proven track record of helping our community afford homeownership. Some benefits of a VHDA home loan include:

Predictable payments with a 30-year fixed interest rate

Small down payments

Free homebuyer classes

Pre-approval availability

Low credit score requirement

Who is eligible for a Virginia Housing loan?

VHDA loans are only available for borrowers who intend to use the home as their primary residence. If you are planning to buy a home as an investment property, second home, use the house for a business, or sublet part of the space, you will not qualify for a VHDA loan.

Borrowers cannot have a net worth greater than 50 percent of the intended home purchase price. Your net worth calculation does not include retirement savings, life insurance plans, or the value of your belongings. Any cash that will be used to help fund your down payment will not be calculated into your net worth.

Income limits as well as home price limits for VHDA loans vary by region across the state. A table outlining these limits can be found on the Virginia Housing website. The maximum VHDA loan limit for a home in the Charlottesville area is $375,000. The two-person maximum gross household income for that area is $90,000. Limits vary by county so check with your lender for more specific amounts.

How do I apply for a VHDA loan?

Only VHDA approved lenders can offer Virginia Housing loans to the community. Approved lenders must comply with strict policies and requirements in order to qualify. Staff must be qualified and experienced with VHDA loans, adhere to Virginia’s fair housing policy, and demonstrate a proven track record of performance. F&M Bank is proud to be an approved VHDA lender.

To apply for a VHDA loan, stop by any F&M Bank location or apply online. To apply online:

The VHDA requires all applicants to complete their homebuyer education class before the loan can be approved. The class can be taken online or in a local classroom. This free class is available to anyone that wishes to learn more about the homebuying process and VHDA loans, even if you are not ready to apply for a loan.

What are the different types of VHDA home loans?

Virginia Housing Conventional

The Virginia Housing Conventional loan is available to both first-time and repeat homebuyers. Borrowers may use the loan to make a home purchase or fund a limited cash-out refinance. The Virginia Housing Conventional loan is a 30-year fixed-rate loan offering the lowest conventional mortgage insurance rates possible. Eligibility includes a minimum credit score of 640, 3 percent down payment, and maximum 45 percent debt-to-income ratio.

Virginia Housing Conventional – No Mortgage Insurance (NMI)

For borrowers with a higher credit score, the VHDA offers their conventional loan with no mortgage insurance. To qualify for the Virginia Housing Conventional – NMI loan borrowers must have a minimum credit score of 660.

Virginia Housing Plus Second Mortgage

If you need help funding your down payment and closing costs, you may consider a Virginia Housing Plus Second Mortgage loan. This option is technically two separate loans – one to pay for your new house and a second mortgage to cover your down payment. Both mortgages are 30-year fixed-rate loans with no prepayment penalties.

Only available to first-time homebuyers, this loan can cover your entire down payment amount as well as your home. At closing, borrowers must have 1 percent of the home purchase price available as cash. Borrowers with a higher credit score (680 or above) can also finance part of their closing costs in the second mortgage. The maximum second mortgage amount is 3 to 5 percent of the home purchase price.

Ready to get pre-approved for a VHDA loan? F&M Bank is an approved VHDA lender. Call us today for help choosing the right Virginia Housing loan. You can also start our online mortgage application or apply in person at your nearest branch.

F&M Mortgage, a division of F&M Bank, has been helping Virginians become homeowners in the Shenandoah Valley for more than a century. Don’t let the mortgage process overwhelm you. Our Mortgage Advisors pride themselves on offering friendly, personalized service, with the kind of local expertise you only find in people who live and work in your community. With VDHA pre approval you can start shopping for the house of your dreams in northern Virginia.

https://www.fmbankva.com/wp-content/uploads/2022/08/1-HEADER-FMVA.jpeg5812000Kristen Durkee/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgKristen Durkee2022-08-29 13:46:052022-09-28 15:41:31Guide to VHDA Mortgages for First-Time Homebuyers